Article by Brad Thompson, courtesy of Business News

BHP says the outcome of union attempts to regain a foothold in the iron ore industry will have a big bearing on whether it pulls the trigger on a potential multi-billion investment in boosting production.

Chief executive Mike Henry says any impact on productivity would make it harder for BHP to justify investment in Western Australia, in another warning from the world’s biggest miner on policy settings in Australia.

In the countdown to the federal election, the BHP boss threw down the gauntlet to Australia’s major political parties to at least keep pace with the investment-positive reforms in other countries and in some cases follow their lead.

BHP has forecast heavy causalities in iron ore as Chinese steel production flattens out and global production continues to increase.

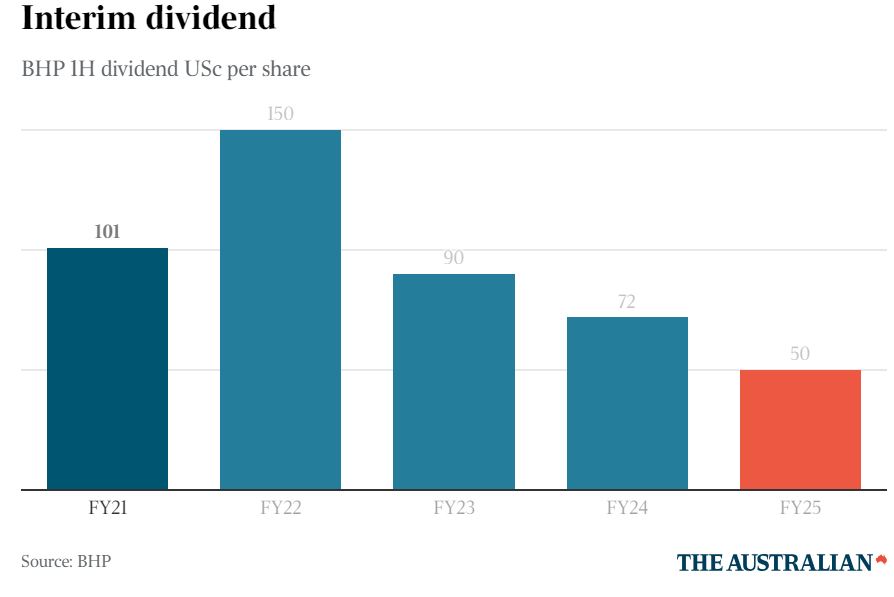

The warning came after BHP delivered its lowest interim dividend since 2017 on the back of weaker commodity prices. The 50c a share dividend was down from 72c a year ago and 90c two years ago.

BHP said it would spend the rest of 2025 assessing the substantial investment required to boost production at its WA iron ore operations to 330 million tonnes a year, with union activity in the Pilbara one of the factors at play.

Unions have forced BHP to the negotiating table under industrial relations changes introduced by the Albanese government, despite assurances that the laws would not affect a sector that has been free of unions and industrial disputes for decades.

Before the IR changes, unions would have had to establish that they represented most workers before BHP was required to negotiate.

Mr Henry said on Tuesday that the company was preparing for a key decision on whether to target 330 million tonnes toward the end of this year.

“We have to keep in mind that the WA iron ore business, ours and others, has been successful based on the policy settings that we’ve had in the past,” he said.

Mr Henry said any impact on BHP investment would depend on the outcome of negotiations, and it was too early to tell how productivity might be affected.

“If the outcome of that negotiation was to take productivity backwards, of course that’s going to make investment less attractive. The projects will compete less well for capital amongst alternative options for BHP or frankly other investors,” he said.

His immediate focus is on the relatively small investment required to get 305 million tonnes a year as BHP continues a strategy to increase exposure to copper in South America and South Australia and potash in Canada.

BHP shipped record tonnes of iron ore from WA in the six months to December 31, but the price it fetched for the steelmaking ingredient plunged 22 per cent year-on-year – from $US103.70 a tonne to $US81.11 a tonne – as the Chinese property market faltered.

Mr Henry reiterated BHP’s view that Australia faced clear economic headwinds and needed to get its policy settings in order as other countries moved aggressively to improve their competitiveness.

“We have been strong advocates for ensuring that we’ve got the right tax settings that are globally competitive, the right energy market policy here that ensures that there’s affordable, reliable energy while staying on track for net zero, and that we’ve got industrial relations policies that promote high levels of productivity,” he said.

Mr Henry said BHP’s call on massive investment to boost copper production at Olympic Dam and nearby mines would depend on labour and power costs and policy certainty.

“We’ll then need to weigh that up against opportunities in Chile, opportunities in Argentina and opportunities in the US,” he said.

“While other countries around the world are taking strong, bold steps to become more competitive … the opportunity for Australia to play for is to lean into that, firstly, to understand that for Australia to maintain and grow standards of living here, for Australia to be successful, it has to be able to compete globally.

“We have to watch the other countries which are moving to become more competitive. And we need to keep pace with that and seek to exceed it.”

In iron ore, BHP noted seaborne supply had outpaced demand in 2024 and kept Chinese port stocks at elevated levels over the past six months.

“New iron ore projects in Africa and potentially some mine restarts are expected to bring further supply pressures from 2026,” it said.

BHP estimates cost support continues to sit in the $US80-$US100/t range for benchmark 62 per cent iron product, with about 180 million tonnes of higher cost supply coming from Australian junior miners, Indian fines and some Chinese domestic mines.

“Over three-quarters of this supply has costs above $US90 a tonne. Export volumes of price-sensitive Indian fines almost halved year-on-year over half-year 2024-25. As the market turns more competitive, some additional high-cost suppliers may leave the market in the coming years,” BHP said.

BHP remained bullish on the copper outlook and on potash, as Mr Henry reassured the market about the potential impact of US President Donald Trump’s trade policies.

BHP reported first-half revenue of $US25.2bn, down 8 per cent on the prior corresponding period, primarily as a result of the decline in realised iron ore and steelmaking coal prices.

Attributable profit rose to $US4.4bn, but underlying attributable profit decreased 23 per cent to $US5.1bn after adjusting for the half year exceptional losses. Some analysts had expected underlying profit to come in at $US5.39bn.

Underlying earnings before interest, taxes, depreciation and amortisation fell 11 per cent to $US12.4bn due to the lower revenue.

Citi analysts led by Paul McTaggart said the EBITDA result was in line with Visible Alpha consensus and 3 per cent ahead of its own estimates.

Analysts at Barrenjoey, led by Glyn Lawcock, also noted underlying EBITDA was in line with consensus and 2 per cent ahead of its own estimates, but “at a segment level, iron ore and coal underlying EBITDA were below expectations while copper was above”.

BHP shares were up 0.2 per cent to $40.87 in a lower market on Tuesday afternoon.